Loan Origination

Streamline application intake, document verification and decisioning with an end-to-end automated process that ensures transparency and compliance.

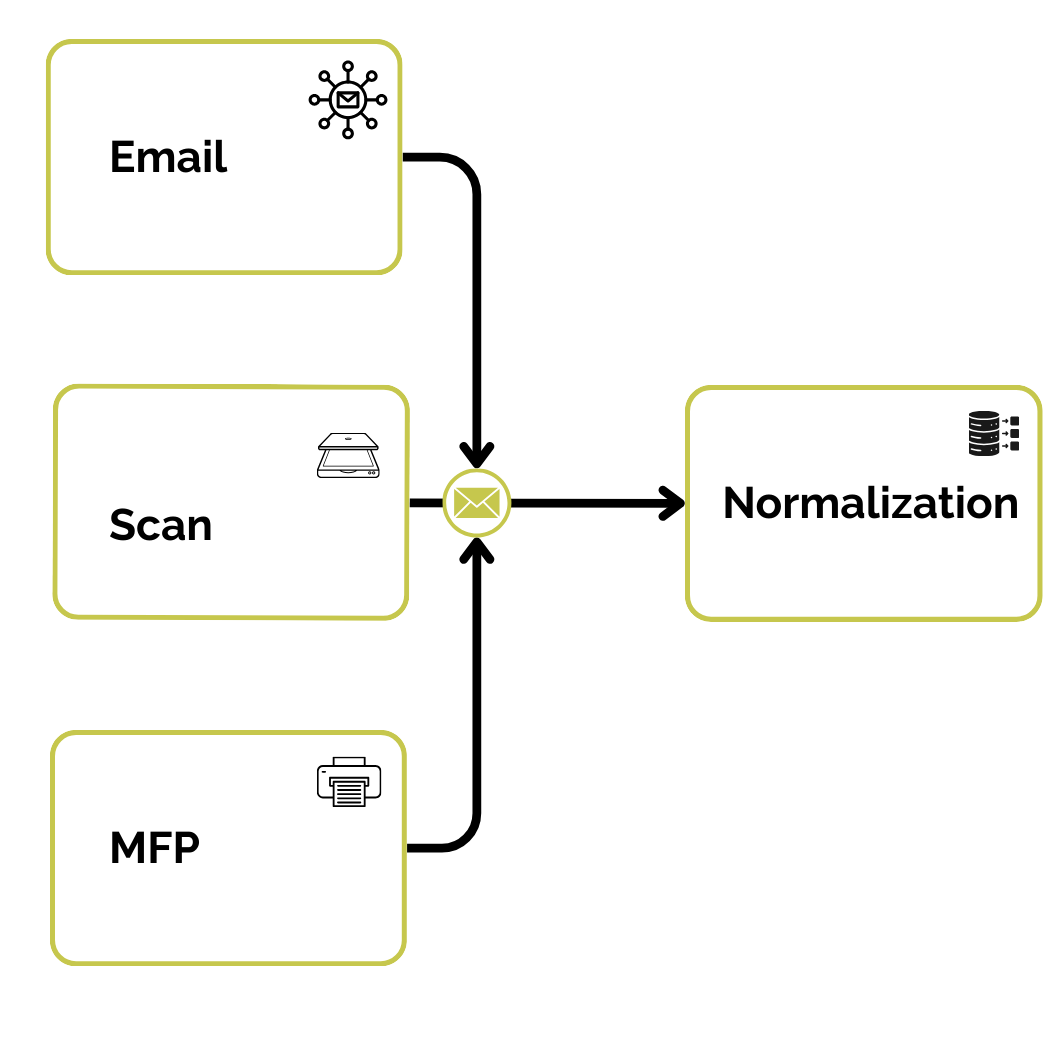

Emails, scans, MFP documents, forms, and customer communications such as account opening documents, loan applications, and KYC materials are normalized into a consistent format before entering your banking workflows.

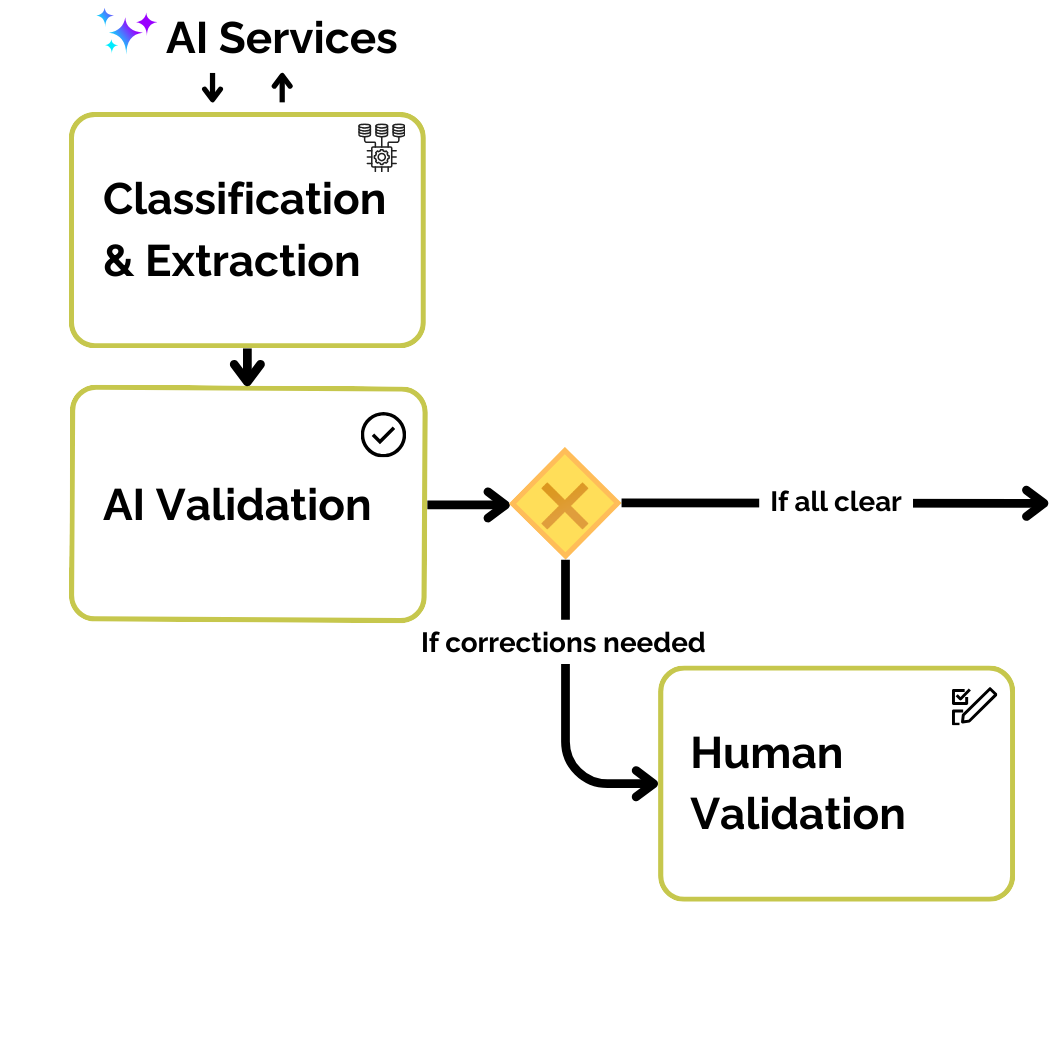

Thanks to intelligent document processing, documents are classified, key data is extracted, and validations are applied for identity, eligibility, compliance, and risk checks so cases can route automatically. Human review is possible when needed.

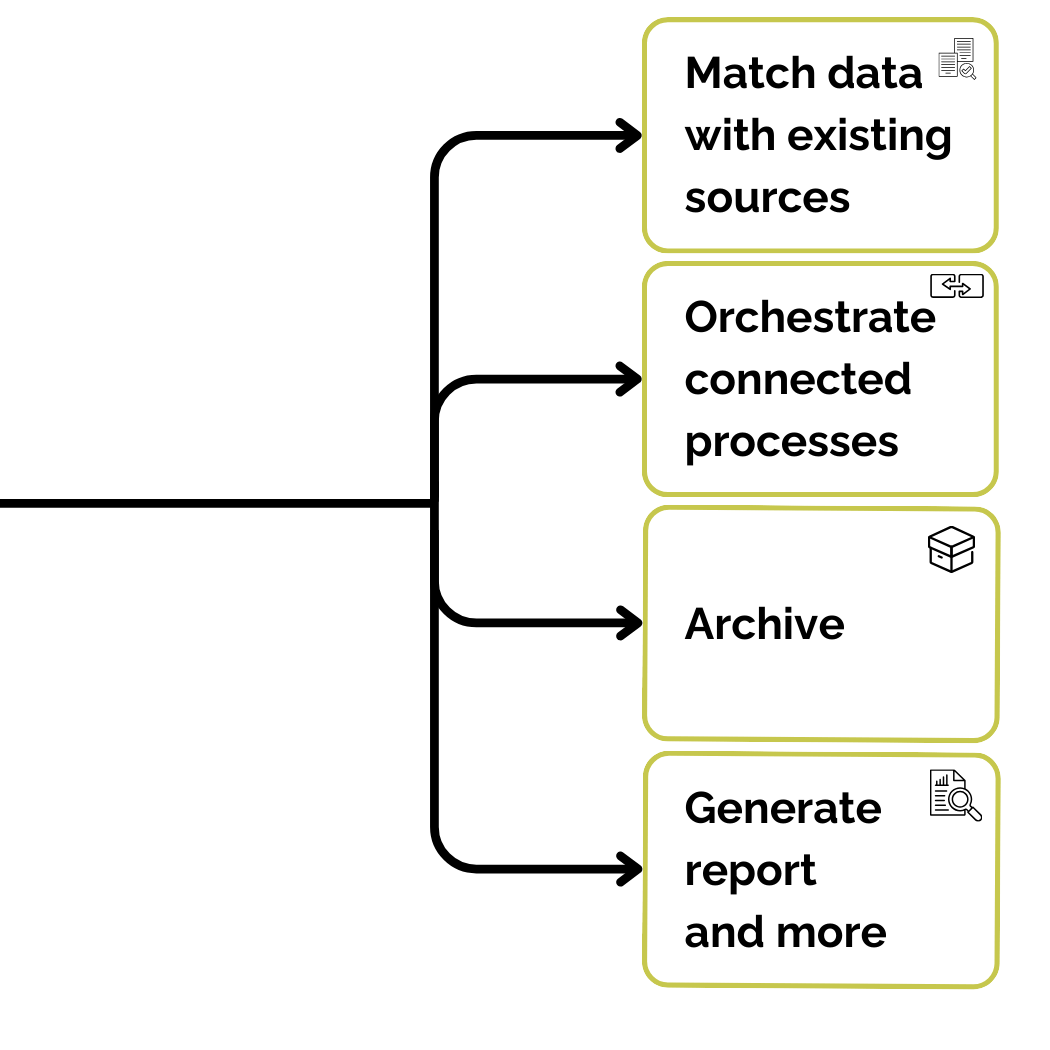

From here, many automated actions are possible, such as sending customer confirmations, opening accounts, progressing loan applications, routing tasks to the right teams, generating reports, and archiving records securely.

Streamline application intake, document verification and decisioning with an end-to-end automated process that ensures transparency and compliance.

Automate document collection, identity verification and eligibility checks to reduce onboarding times and enhance your customer’s experience.

Route inbound requests (emails, documents, forms, call center recordings) to the right teams faster with intelligent triage and data extraction.

Capture and process supporting documents, trigger alerts and automatic activity logging ensures you are always audit-ready.

Pre-built, customizable solution templates for rapid time-to-value.

Modern banking requires more than just innovation – it requires confidence in how innovation is implemented. With OCTO, banks can take full advantage of advanced AI services while maintaining control, transparency and compliance.

Whether integrating large language models for document understanding or automating decision-making across loan and compliance processes, OCTO’s orchestration capabilities ensure every component – AI or not – is governed and auditable.